5 Critical Checklist Items for a Flawless 2030 Retirement

If you are targeting a 2030 retirement, you are officially four years away from liftoff and it is time to stress-test your financial trajectory. In this episode, Dr. Chris Mullis maps out a comprehensive countdown checklist to transition smoothly from accumulating wealth to safely spending it. Tune in to discover how to navigate the pre-Medicare healthcare bridge, master late-career tax windows, and optimize your Social Security benefits for a flawless launch.

Retirement Big Picture

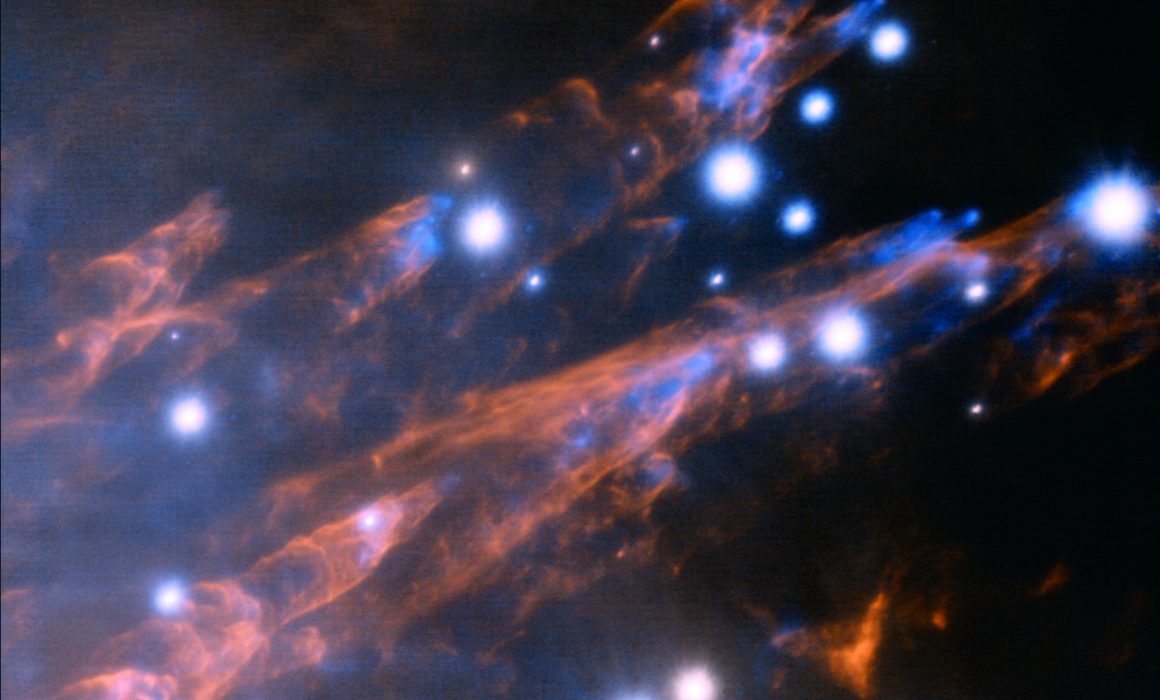

This segment takes listeners 1,500 light-years away into the Orion Nebula to examine the stunning visual phenomena of the “Orion Bullets,” which were first discovered by astronomers in 1983. The actual astronomical image captures dense, supersonic clumps of gas ten times the size of Pluto’s entire orbit tearing through neutral hydrogen clouds at a staggering 250 miles per second. Captured by the professional Gemini North telescope using a specialized near-infrared camera to peer straight through interstellar dust, these high-speed projectiles leave behind brilliant, trillion-mile-long glowing hydrogen wakes that mimic supersonic tracers.

Image Credit: International Gemini Observatory/NOIRLab/NSF/AURA

Sign Up for The Launch

The Launch is a weekly email from Dr. Chris and his team. It’s full of retirement tips, news, listener questions & more, straight from us to your inbox. Get smarter about retirement in just 5 minutes every week. Let’s go!

Episode Resources

- 5 Things to Do Today If You Want to Retire in 2030 — Christine Benz and Margaret Giles

Episode Transcript

Introduction

Dr. Chris Mullis, PhD, CFP®: Imagine you’re standing on the launch pad, looking at a departure date just four years away in twenty thirty. You’ve spent decades accumulating fuel for your nest egg. But as the countdown narrows, how do you ensure your portfolio doesn’t face a rough reentry?

Today, we’re breaking down the ultimate four-year checklist to transition smoothly from saving wealth to safely spending it. Are you ready?

NASA: 3, 2, 1, 0 and lift off. Lift fell Americans return to space as discovery clears the tower.

Dr. Chris Mullis, PhD, CFP®: Welcome back to Retirement Isn’t Rocket Science. This is episode 18. I’m your host, Dr. Chris Mullis. I spent my first career as an astrophysicist mapping the far reaches of the cosmos with NASA’s space telescopes. Now, as a certified financial planner with 21 years of experience, I help you navigate the universe of retirement.

Our mission is clear: lower your taxes, strengthen your portfolio, and give you the confidence and the capacity to spend more. Buckle up. We’re gonna master your money and explore the mysteries of the universe along the way

In today’s show, four years to liftoff. What is on your mission checklist for a twenty-thirty retirement? And the power of thirty-five. Why your career timeline dictates your retirement paycheck when it comes to Social Security. And finally, cosmic tracers, the supersonic bullets reshaping the Orion Nebula

Retirement Briefing Room

Dr. Chris Mullis, PhD, CFP®: Welcome to the Retirement Briefing Room. This is where we huddle up to take a close look at important aspects of your financial life, spotlight pathways of success, and think about how to integrate these into your retirement mission plan

Today, our core flight plan is built around the insights from a recent Morningstar interview featuring Christine Benz, the director of personal finance and retirement planning for Morningstar, and the interview was conducted by Margaret Giles. Christine Benz is widely regarded as one of the most practical and authoritative voices in wealth management, specializing in sustainable decumulation and helping diligent savers navigate the critical transition into retirement

If your retirement date is twenty thirty, you are four years away from liftoff. In rocket science, the final years before launch aren’t about building a brand-new rocket from scratch.

They’re about rigorous stress testing, stabilizing the systems, and calibrating the trajectory. The exact same rules apply to your wealth. Today, we’re covering the five things you need to tackle right now to ensure a flawless transition. Let’s dive into that checklist. Number one: track and tame your real-world spending runway.

Christine points out that tracking your spending is the absolute baseline starting point for any viable retirement plan. It is the raw main ingredient you need for an accurate projection

If you don’t know what you’re spending today, you can’t accurately map out what you’ll need tomorrow. Christine suggests moving away from the old paper and pencil accounting and experimenting with modern budgeting apps like Monarch Money or You Need a Budget.

If apps aren’t your style, she notes you can review your year-end credit card statements to see expenses grouped by major categories

The number two on your checklist is to secure your income floor and your safety buckets. Once you know your numbers, you have to defend them against what we all call sequence of returns risk.

That’s the danger of a market crash right when you begin taking withdrawals. Christine recommends establishing a bulwark of assets that you can spend from early in retirement if equities aren’t cooperating. Her ballpark recommendation is to hold anywhere from five to 10 years worth of portfolio expenditures in the combination of cash and high quality, short to intermediate term bonds

In my retirement firm, we take a similar approach, but there is one important difference. Our war chest or retirement income runway tends towards the lower end of Christine’s range. We like to see three to five years of income outside of stocks. This sizing is appropriate with dynamical spending rules or a guardrails approach to portfolio withdrawals

Number three on your checklist is to evaluate the role of work and practice your transition. Retirement isn’t just a math problem. It’s a profound psychological shift. Christine is a huge advocate of gradually segueing into retirement if you can.

Continuing to earn even a small part-time income stretches out aspects of your job you enjoy, alleviates portfolio withdrawal pressures, and gives you a continued sense of purpose, identity, and mattering as you age. We focus heavily on this behavioral blind spot in my practice, warning against the retirement hell.

That’s the sudden onset of boredom and anxiety that hits when you instantly inherit forty to fifty hours of free time each and every week. We guide our clients to intentionally build routines, volunteer commitments, or a social group before their employment ends, so they don’t face an identity crisis when they walk away from a lifetime career

Number four on the list is to calibrate your portfolio burden and income streams. This is about putting a finer point on your guaranteed non-portfolio income. Christine explains that you should take stock of sources like Social Security and pensions. By subtracting these guaranteed sources from your total spending number, you arrive at the actual burden or the amount you must pull from your investment portfolio.

Furthermore, she notes that delaying Social Security often makes excellent sense if you have an average or long life expectancy, even if you have to tap other sources to tide you over early on

The last item on your checklist, number five, is mastering the tax window and your healthcare bridge. Those four years leading up to retirement require aggressive forward-looking tax and estate planning. Christine points out that even dedicated do-it-yourself investors should get a professional set of eyes at this juncture to evaluate tax strategies and determine which silo of assets to pull from and when.

Let me expand on this by highlighting several major financial hurdles that should be considered in this four-year window leading up to your retirement. First, the pre-Medicare healthcare bridge. If you retire by twenty thirty but are under sixty-five, you must treat health insurance as a discrete, high-cost temporary expense.

This might come from the ACA exchange or from a COBRA extension of your previous employer’s health insurance. You need to arrange your asset locations now so you can intentionally manage your modified adjusted gross income to qualify for ACA tax subsidies later

The second item on my list is the low-income tax window. Your final working years are your peak earning years, meaning you are in a high tax bracket. I want to highlight the tax window, the low income gap between the day you stop working and the day you hit required minimum distributions or claim Social Security. Use your current runway to plan multi-year Roth conversions that you will execute the moment your wage income drops

Number three on my list, the two-year IRMAA look-back. I want to point out a massive blind spot. Medicare premiums and IRMAA surcharges are calculated based on your tax returns from two years prior. If you retire in twenty thirty at age sixty-five, your income from twenty twenty-eight directly dictates your healthcare costs.

You must carefully time late career asset sales or stock option exercises to avoid crossing an IRMAA cliff. And let’s just define our acronyms. IRMAA is the income related monthly adjustment amount. These are higher Medicare premiums you may face depending on your income level just before and in retirement.

The final item on my extra list is the legal clock.

Although most of our listeners are likely super savers, some may need to insulate assets like a family home from potential long-term care or nursing home costs, but you must act early. Medicaid enforces a strict five-year look-back period on asset transfers

in most states, making the four-year pre-retirement runway the prime time to consider establishing defensive legal guardrails

As we bring this to a close, remember, retirement planning isn’t a static calculation you set and forget.

It’s a dynamic process of adjusting the controls as the environment changes. By tackling your spending, securing your short-term cash flow, and mapping out the upcoming tax and healthcare windows today, you aren’t just crossing your fingers for twenty-thirty. You are ensuring a stable, predictable, and deeply fulfilling launch into your next great adventure

If you wanna bring a professional team into your orbit today to ensure all of these variables are completely aligned before you leave the atmosphere of your career, visit retirementisntrocketscience.com and click Work With Dr. Chris. Now, let’s head over to mission control to answer your financial questions and get you retirement ready

Discovery Houston, 20 seconds to LOS. Tres Hothead. Nice to be in orbit.

Ask Mission Control

Welcome to Ask Mission Control. This week’s question comes from Henry. Henry asks, “Is Social Security based on my thirty-five highest earning years?” The short answer, Henry, is a resounding yes. The Social Security Administration looks at your entire work history. But when it comes time to calculate your actual monthly benefit check, they only look at your top thirty-five years of earnings.

But as we always say here on the show, while retirement isn’t rocket science, the mechanics under the hood of these government programs do have a few moving parts. Think of your thirty-five year earnings history like a flight log of a long-duration space mission. Every year represents a vital data point. If you have empty spaces in that log, it alters your entire trajectory.

Let’s break down exactly how this calculation works and why it matters immensely for diligent savers who are approaching or navigating early retirement

Number one, the inflation smoothing factor. The government doesn’t just look at what you made back in nineteen ninety and compare it directly to what you made last year. Instead, they use a process called indexing to adjust your past earnings for inflation.

This brings your historical wages up to today’s dollar values so they can compare your earnings over time on an equal playing field. Once they’ve indexed your entire career history, they line up every single year from highest to lowest and pull out the top thirty-five

Number two, let’s look at the danger of the zero-year trap. What happens if you don’t have thirty-five years of earnings? This is where many successful savers get tripped up, particularly those who want to cross the retirement finish line early, say at age fifty-five or sixty

Let’s look at the math. If you have only worked for thirty years, the Social Security formula doesn’t just average those thirty years. The system is hard-coded to divide your total career earnings by thirty-five years, or specifically four hundred and twenty months. So what’s the impact?

This means those five missing years are entered into the calculation as zeros . Those big fat zeros act like a gravitational pull, dragging down your average indexed monthly earnings and shrinking your eventual baseline check. Conversely, if you worked forty years, the formula automatically discards your five lowest-earning years.

This is fantastic news because those early lower-paying jobs you had in your late teens or twenties completely disappear, replaced entirely by your peak earning years

The third aspect we wanna look at is fitting the pieces into the grand design. For our listeners who built up multi-million dollar nest eggs, Social Security isn’t your main source of fuel, but it is an important inflation-protected piece of your broader income plan. Maximizing it requires looking at the whole financial chessboard.

We need to think about tax management. Social Security benefits can be taxed on up to eighty-five percent of the payout depending on your overall provisional income. If you retire early and have a gap before collecting Social Security, that may be the ultimate golden window to execute Roth conversions at historically low tax brackets

the second aspect within this dimension is the investment portfolio coordination. Should you draw down from your traditional IRAs early to allow your Social Security benefit to grow by eight percent per year until age seventy? Or should you preserve portfolio longevity by claiming earlier?

The third subcomponent for us to think about is estate and legacy planning. For married couples, the higher-earning spouse maximizing their benefit provides a crucial insurance policy for the surviving spouse, as the surviving spouse will inherit the larger of the two monthly paychecks from Social Security.

So remember that very easy to understand rule of thumb here. When one spouse passes away, the larger of the two Social Security checks remains

So in diving into Henry’s question, we’ve looked at first, the inflation smoothing factor. Number two, the danger of zero years, and number three, fitting those pieces into your grand design when it comes to tax management, your investment portfolio, and your estate and legacy planning, specifically actually guarding the surviving spouse’s income.

So that is a lot because of all those pieces, right? Taxes, investments, government benefits, these are all deeply interconnected. A certified financial planner can build a customized dynamic model of your specific career trajectory.

They can tell you precisely how much a single extra year of consulting work might boost your lifetime benefit, or how to bridge your income gap cleanly without triggering a massive tax bill or higher Medicare premiums.

Henry, thank you again for this Social Security question. That’s a, on the surface, a simple question, but has a lot within it. So thank you for letting us open that door and explore that important question together. If you’ve got a retirement question that you’d like us to answer on the show, head over to retirementisntrocketscience.com and click ask a question.

Or even better, you can skip to the front of the line by calling Mission Control at seven zero four two three four six five five zero and record your audio question. Now let’s look at cosmic bullets slicing through thick gas clouds at supersonic speeds in the famed Orion Nebula

NASA: In Discovery Houston, we’ve got a good picture of Steve.

Retirement Big Picture

Dr. Chris Mullis, PhD, CFP®: Imagine looking up at the winter sky and seeing the peaceful, familiar constellation of Orion. It looks static, calm, and unchanging. But deep within its core, a cosmic shooting gallery is taking place, with supersonic bullets 10 times the size of Pluto’s orbit tearing through space at a staggering 250 miles per second.

Today, we look at how the universe handles massive momentum and what happens when cosmic forces collide. Welcome to the Retirement Big Picture part of our show. This is where we look up and look out to expand our appreciation and understanding of our amazing universe. A long time ago in a galaxy not far, far away, I spent nearly two decades studying the cosmos as an observational astrophysicist.

This is a topic that I fell in love with in seventh grade and still love it dearly. So thank you for joining me in this exploration together. Today we’re setting our coordinates for one of the most famous and highly studied regions in our night sky. That is the Orion Nebula. Located roughly 1,500 light years away from us, it’s a massive stellar nursery where new stars are constantly being born. But recent data from the International Gemini Observatory, alongside insights from NASA’s premier space telescopes, have given us a front row seat to a jaw-dropping phenomena known as the Orion Bullets

We first found these high-speed cosmic projectiles way back in 1983. Astronomers peering into the deep infrared wavelengths noticed something peculiar on the outskirts of the Orion Nebula. They found dense supersonic clumps of gas being violently ejected from deep within the nebula’s core

They quickly earned the nickname Orion Bullets because of the unmistakable visual patterns they leave behind. As these highly concentrated clumps of gas rifle through the surrounding neutral hydrogen cloud, they heat it up intensely. This process creates distinctive tubular and cone-shaped wakes.

To the eye of a powerful telescope, these wakes shine brightly like glowing tracers tracking a bullet fired across a dark room. And when I say these bullets are big, I mean astronomically big. Each individual gas bullet is roughly ten times the size of Pluto’s entire orbit around the Sun. Imagine a projectile that’s massive, traveling at speeds of up to two hundred and fifty miles per second. That’s nine hundred thousand miles per hour. The wakes left behind these bullets are even more staggering, spanning up to a fifth of a light year in length. That’s over a trillion miles of glowing, energized hydrogen gas tracing their paths

You might be wondering what on earth, or rather what in the cosmos, could possibly possess enough energy to shoot chunks of gas the size of solar systems out into space at supersonic speeds? The violence causing this is likely related to the recent formation of a cluster of massive stars.

When these giant stars ignite, they produce incredibly powerful stellar winds and intense radiation fields. Less than a thousand years ago, which is a mere blink of an eye in cosmic time, a violent star formation event acted like a cosmic cannon expelling these gas clumps at very high velocities.

Let’s bring this back down to earth for a moment. Can you actually go out and see this? The answer is a definitive yes and no. So the constellation is easy, right? The Orion Bullets live within the constellation Orion the Hunter, and Orion is one of the most recognizable and brilliant constellations in our sky.

It is beautifully visible from all across the United States, especially during the winter months. You can easily spot his iconic three-star belt shining brightly in the night sky. I have memories of being a small child and being on road trips and, and having my head against the window and looking out and seeing Orion’s Belt.

It has to be the first pattern in the sky that I could recognize as a small child. So it is easy to see and it’s beautiful. So there is a big difference between our views as amateur skywatchers and professional skywatchers. If you’re an amateur astronomer with a pair of good binoculars or a backyard telescope, you can easily view the Orion Nebula itself.

It looks like a beautiful ghostly green-white smudge just below Orion’s Belt in what we call his sword. However, the Orion Bullets themselves are a different story because they are shrouded deep within the thick clouds of interstellar dust, they are completely invisible to the naked eye and backyard optical telescopes.

To actually see the bullets, you’ll need to have heavy artillery of professional ground-based observatories equipped with specialized technology. To capture the stunning images we have today, the Gemini North telescope in Hawaii used its near-infrared camera or NIRI to peer straight through the dust.

Let me tell you a little story about Gemini North. This is a massive eight-meter telescope on the summit of Mauna Kea on the Big Island of Hawaii. Now, I spent many, many years observing at that location, which is the world’s best location to do astronomy. Now, I was doing my PhD with a number of telescopes, but I did not use the Gemini North because it was still under construction during my grad school years.

But that’s where the story comes in. We’re at the world’s best site, and many times over that construction phase, I had to call up the construction team that was building the Gemini North telescope to ask them to turn off the lights when they leave each day. So many times I would have to leave my observatory, go over to the Gemini North location that was being constructed, and turn the lights off.

It’s a fun story now, but it was frustrating back then because the time is very tight on the night sky each night, and we have a lot of work to do. So having to get out, go outside, turn off someone else’s light switch in the world’s best location felt a little crazy, but it’s fun now. But kudos to Gemini North for keeping the lights off now that they are on the sky and taking beautiful images like the Orion Bullets.

looking at these images of the Orion Bullets, it’s a vivid reminder of how dynamic and high velocity the universe really is. Things are constantly moving, changing shape, and generating massive momentum. And if you think about it, building a retirement nest egg has a very similar trajectory.

For thirty, forty, sometimes even fifty years, you are in your high-energy star formation phase. You are working hard, diligently saving, and building a multi-million dollar portfolio. You’ve built up incredible momentum. But just like those massive stars in Orion, that much accumulated energy creates a lot of complexity.

When you have a nest egg of two million or five million or even more, the financial winds around you, like tax management, required minimum distributions, market volatility, estate planning, they all start moving fast. Suddenly, you realize the strategy that got you to retirement isn’t the same strategy that will get you through retirement.

The universe is full of complex, fast-moving parts, but planning for your next great adventure doesn’t have to feel overwhelming. You’ll find the Gemini North image of the Orion Bullets in this week’s newsletter called The Launch. If you aren’t already receiving this powerful resource each week with insights beyond what you hear on the podcast, you should sign up for it at retirementisntrocketscience.com

Conclusion & Action Items

Dr. Chris Mullis, PhD, CFP®: We’ve spent today focused on this question: Are you ready to shift trajectories? Five steps to take today if you plan to retire in four years. Now, it’s time to open the hatch. This is your spacewalk. You’re stepping out of the routine and into the bright light to overlay today’s insights on your plans to worry less and retire more.

This isn’t just a stroll. This is where the work gets done. To move from theory to better real-world outcomes, here are your next mission objectives. Number one, audit your baseline trajectory. Spend the next month using a budgeting app or reviewing the last twelve months of credit card statements to isolate your true base great life spending number.

Number two, calculate your portfolio burden. Deduct your projected guaranteed non-portfolio income streams like Social Security and pensions, and deduct them from your baseline spending to figure out the exact annual distribution stress on your investments

Number three, map your healthcare and tax timelines. If you plan to retire before age sixty-five, model your pre-Medicare insurance costs, analyze your exposure to the two-year IRMAA look back, and draft a multi-year Roth conversion schedule

And finally, log into your personal account ssa.gov and download your full earning statement. Check the total number of working years you have on record. If you’re planning on an early retirement and have fewer than thirty-five years of substantial earnings, have your financial planner calculate the exact dollar impact those zero years will have on your lifetime cash flow I challenge you to take one idea from today’s show and put it into practice this week to make your retirement even better. Thank you so much for joining me. Remember, you’ve done the hard work of savings. Now let’s do the smart work of planning. Until next time, keep your eyes on the horizon, enjoy the adventure.

You are go for retirement!

Credits

Dr. Chris Mullis, PhD, CFP®: We thank the National Aeronautics and Space Administration for providing the radio communications between the space shuttle astronauts and the flight controllers.

Disclaimer

This show is for informational and entertainment purposes only. It is not specific tax, legal, or investment advice. Before considering acting on anything you hear in this show, first consult with your own tax, legal, or financial advisor