Probate Isn’t the Boogeyman?

In this episode, Dr. Chris challenges the ultimate retirement “boogeyman” by explaining why probate isn’t a mission failure, but a strategic tool for protecting your legacy. We’ll also clear the air regarding the headlines about the Iran conflict and the US dollar, helping you distinguish between real risks and “financial pornography.” Finally, we’ll look 300 million light-years away to the Coma Cluster to see how the invisible forces of the universe mirror the hidden risks in your retirement portfolio.

Retirement Big Picture

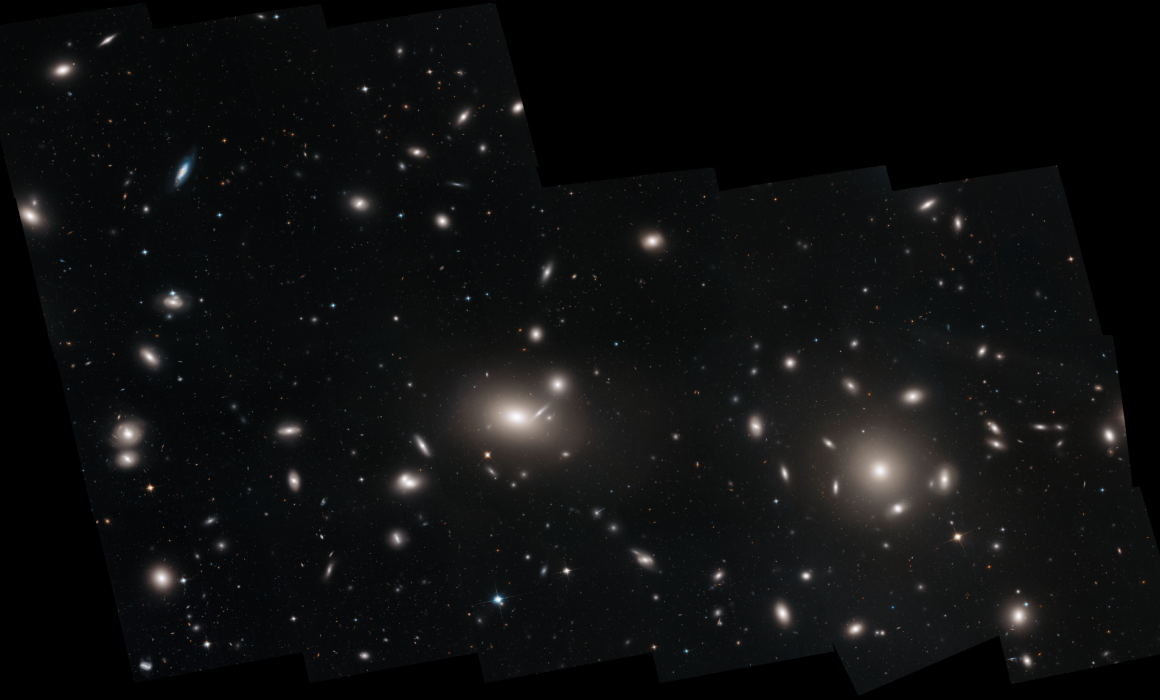

This segment explores the Hubble Space Telescope’s massive census of 22,000+ globular star clusters within the Coma cluster, a “city of galaxies” located 300 million light-years away. Dr. Chris compares these ancient, tightly packed “cosmic snow globes” to core blue-chip investments, noting they serve as tracers that reveal the location of invisible dark matter. Just as dark matter provides the hidden gravity that keeps galaxies from flying apart, invisible financial forces like inflation and tax law changes are the “dark matter” of your portfolio that require expert navigation.

Image Credit: NASA, ESA, J. Mack (STScI), and J. Madrid (Australian Telescope National Facility)

Sign Up for The Launch

The Launch is a weekly email from Dr. Chris and his team. It’s full of retirement tips, news, listener questions & more, straight from us to your inbox. Get smarter about retirement in just 5 minutes every week. Let’s go!

Episode Resources

- What Issues Should I Consider Before Closing The Estate — Dr. Chris’ 25-point checklist

- Don’t “Avoid Probate”: Reframing Estate Planning Success Around Managing (Not Escaping) The Probate Process — David Haughton, JD, CPWA®

Episode Transcript

Introduction

Dr. Chris Mullis, PhD, CFP®: In the world of rocket science engineers work tirelessly trying to avoid friction because friction generates heat and slows us down. In retirement planning, most people treat the P word probate as the ultimate source of friction. We’re told to avoid it at all costs. Run for the hills and build complex trust

fortresses to escape it. But what if I told you that probate isn’t a mission failure? What if in some cases it’s actually the heat shield that protects your legacy? Are you ready?

NASA: 3, 2, 1, 0 and lift off. Lift fell Americans return to space as discovery clears the tower.

Dr. Chris Mullis, PhD, CFP®: Welcome back to Retirement. Is it Rocket Science? This is episode 15. I’m your host, Dr. Chris Mullis. I spent my first career as an astrophysicist, mapping the far reaches of the cosmos with NASA space telescopes. Now as a certified financial planner with 21 years of experience, I help you navigate the near universe of retirement.

Our mission here is clear, lower your taxes, strengthen your portfolio, and give you the confidence and the capacity to spend more. Buckle up. We’re going to master your money and explore the mysteries of the universe along the way.

Dr. Chris Mullis, PhD, CFP®: In today’s show is avoiding probate actually a mistake for your retirement mission plan. A listener audio question asks about the impact the Iran war and what we should be doing in response to it and reaching for the old stars. How 22,000 ancient star clusters reveal the hidden structure of the universe and your portfolio.

Retirement Briefing Room

Dr. Chris Mullis, PhD, CFP®: Welcome to the Retirement Briefing Room. This is where we huddle up to take a close look at important aspects of your financial life, spotlight pathways of success, and think about how to integrate these into your retirement mission plan. Today we are diving into a provocative piece titled Don’t Avoid Probate Reframing Estate Planning Success Around Managing, not Escaping the Probate Process.

It was published on kitsis.com and the author is David Houghton. David serves as the Vice President of Estate Planning at Carson Group and brings a deep legal background as a member of the Massachusetts and New Hampshire bars.

Let us begin with the myth of the boogeyman. In my previous life as an astronomer , we lived by the data. If the data said a certain trajectory was necessary, we didn’t call it bad. We called it the flight plan. Yet in estate planning we’ve labeled probate as a failure.

David points out that many clients come to the table with a singular, almost obsessive goal. Avoid probate at all costs. But here’s the reality, check. Probate is not a punishment for failing to plan.

It is simply the statutory estate plan that applies to every resident of your state. If you don’t write your own plan, the state legislature has already written one for you. Probate is the infrastructure that clarifies who owns what, who has the authority to act and how to resolve claims so that your estate can be settled with finality.

Next, let’s look at the great will paradox. We want to clear up a massive misconception that I hear almost every week in my practice. Many people believe that if they have a last will and testament, they have avoided probate friends .

I hate to be the one to tell you this, but having a will actually ensures that probate occurs. Think of your will not as a get outta court free card, but as a set of instructions for the judge. A will has no legal authority on its own. It requires the court to validate it and give the personal representative the power to move your money.

So what do those mechanics look like? What actually happens if you find yourself in the probate process? It generally follows a five step trajectory. Step one, the petition you file with the court to open the estate and appoint a representative. Step two, the authority the court gives that representative the formal power to act.

Step three, the inventory. You identify every asset, get valuations and notify anyone who might be interested, including creditors. Number four, the cleanup you pay, the debts, taxes, and expenses of the estate. And number five, the launch. Only after everything else is cleared, do the remaining assets get distributed to your heirs.

Many of you listeners have built revocable trusts to bypass this court process. And while that works, to keep things out of the public eye, don’t confuse avoiding probate with avoiding work. David calls trust administration, a private form of probate. Your successor trustee still has to value the property, identify the assets.

Pay the final bills and deal with the IRS. The difference isn’t the complexity, it’s the visibility. It happens in a lawyer’s office rather than in the courtroom.

Many people are very surprised to hear that even perfect plans end up in court. You might have a five-million-dollar perfectly structured trust, but you can still end up in probate. Why is this? It’s because life is complicated and life is dynamic. Here are some things I see out in the real world that often bring a surprise date with probate. Number one, the late arriver asset. Perhaps you bought a new vacation home. Or you opened a new brokerage account and forgot to title it in the name of the trust, or number two, the dreaded refund check, A tax reimbursement, or a final compensation check comes in after you pass away, made out to you personally.

You can’t deposit that into a trust account without opening a probate estate to get the authority to sign it. And number three, the digital ghost. Your Bitcoin, your social media accounts or your intellectual property might not have a clear transfer process. So these Are just three examples of the multitude of gotchas that can sneak up and cause you to have to probate an estate despite doing a lot of intentional and thoughtful planning ahead of time to avoid it.

All that said, there are times when probate is actually preferred. Yes, there are times when you want the court’s help. Here are two typical situations where , I think it’s very helpful to have court collaboration. Number one is a situation of family conflict.

If your heirs get along, like a pack of stray cats, having a judge provide procedural guardrails. Can prevent a total meltdown. The second situation is creditor protection. In some states, probate creates a strict one year statute of limitations for creditors to make a claim.

Once that year is up, the door is locked. If you do everything privately, you might not get the same level of finality and beneficiaries might worry about a clawback years in the future.

You might be wondering what is the role of a financial planner when it comes to estate planning?

At my retirement and tax planning firm. We are not attorneys and cannot prepare legal documents and certainly cannot give legal advice or practice law. But we have reviewed hundreds of estate documents and have helped many families navigate these complex and transformative decisions.

We will act as your advocate and interpreter when consulting with attorneys, making sure your wishes and your situations are thoroughly understood. And translating their legalese into plain English. More specifically, we will help you understand what estate planning documents you need. Think through your choices and decisions.

Meet with your attorney to help you get the documents drafted. Update your financial accounts and beneficiaries to reflect this plan. Conduct family meetings if it’s desirable, to help your family understand the hows and whys of your plan. And by the way, I think this is a huge missed opportunity for so many families to clearly communicate what’s to be expected and the intentionality behind it.

Super important. Then also critical to success , review all of this periodically to make sure your estate plans remain up to date. Fully aligned with your wishes. And then this last one is huge and it’s a heavy one. My role is to ensure your legacy is smoothly passed to the people and causes you love by providing them with critical support when you’re gone.

So you can see, success in estate planning isn’t just about a document that stays in a drawer. It’s about coordinating. It’s about ensuring that when the time comes, your family isn’t met with a shocking surprise, but a well-managed transition. If you’re responsible for closing a estate for someone, for example, a parent or close friend, I have created a checklist that covers 25 of the most important planning issues to identify and consider before closing that estate.

It includes cashflow, assets, and debt, additional administration issues. Tax issues. You’ll find this free resource in the weekly newsletter called The Launch that you can sign up for by visiting retirement isn’t rocket science.com

Remember, your estate plan is a lot like a Rockets guidance system. It’s not just about the launch. It’s about every midcourse correction along the way. Probate isn’t a sign that your mission failed. It’s just one of the possible flight plans. The goal isn’t to escape the legal system, but to ensure your family has a clear stress-free map to follow when you’re no longer at mission control.

You’ll find a link to David’s article in the show notes and on our weekly newsletter. Now let’s head over to Mission Control to answer your financial questions and get you retirement ready.

Discovery Houston, 20 seconds to LOS. Tres Hothead. Nice to be in orbit.

Ask Mission Control

Welcome to Ask Mission Control. Imagine this, you’re on a long distance space flight and you hear a rumor that the ship’s oxygen system might be replaced with a different brand halfway through the trip. It sounds terrifying, doesn’t it? But before you start holding your breath, you have to ask, is the new system even built yet?

Does it actually fit the pipes? That’s the gist of this week’s listener question. And yes, it’s an audio question

Hello, mission Control. This is Brett from, , Los Angeles, California. , I have been paying attention to this, , to this war in Iran. , And I am seeing things about how the current or might shift use of the dollar as the oil trading currency to Euros or yuan or other currencies. And , the implication is that would lead to a lot of inflation.

, I’m wondering how we should be thinking about this. I suspect that running out and buying a bunch of euros isn’t the right answer. . I look forward to hearing your response. Thank you.

Dr. Chris Mullis, PhD, CFP®: Brett, first off, thanks for reaching out. You are definitely not alone on this. Every time we turn on the news and see geopolitical shifts, whether it’s a conflict in the Middle East or shifting alliances, the headlines start screaming about the end of the dollar and the rise of the yuan and the Euro , it feels like the equivalent of a solar flare heading straight for our retirement nest eggs. As a former scientist , I’ve spent a lot of time thinking about systems and stability in the financial world. The US dollar isn’t just money

it is the operating system of the global economy. Think of it like Microsoft Windows in the nineties, even if you didn’t like it, every business, every bank and every oil contract ran on it. Could The world switch to a different os. Sure. That requires a rewiring of every single computer, training every user, and trusting that the new software won’t crash when things get bumpy

Now, Brett, you mentioned the petro dollar, the idea that oil is traded in dollars. People fear that if Saudi Arabia or other nations start taking you on or euros, the dollar will come screaming back to our shores like a booster rocket with no parachute causing hyperinflation.

But let’s think through this together, beginning with the mechanics . For the dollar to lose its status, there has to be a viable alternative. Right now the Euro has its own internal family, squabbles and the yuan . Well, the Chinese government controls its value so tightly that most global investors don’t trust it to be the World’s Bank just yet.

And I’m afraid that media, as it very often does, is feeding us financial pornography, those sensational headlines designed to make you click and panic. The reality is that currency shifts are more like tectonic plates moving than a vase breaking. It happens over decades, not days.

So how do we think about this in terms of our portfolios in general? I would tell you that we don’t build a retirement plan based on a crystal ball. We build it to be flexible and adaptive. If you’re worried about inflation, whether it’s caused by currency shifts or just government spending, you don’t run out and buy euros.

Why not? Because if the dollar is in trouble. The global economy is likely in a tailspin, and the euro won’t be a safe harbor. It will be in the same storm instead, I would point you towards. Diversification, for example, in the portfolios that we manage for our clients. At my retirement and tax planning firm, we have a healthy mix of US and non-US equities.

When you own a piece of a company in France or Japan, you effectively own a currency hedge. Because those companies earn in Euros or yen, this provides a natural structural hedge against the weakening dollar without the high fees and the risks of direct currency speculation

From an income standpoint, we want to make sure your lifestyle, your groceries, your travel, your golf, your projects are funded by reliable sources. If inflation does tick up, we want to own real assets. This means stocks of companies that have the power to raise prices when their costs go up.

If the price of bread goes up, the company making the bread still makes a profit.

I think the biggest risk to your nest egg isn’t actually a global currency shift. It’s emotional decision making. Selling your domestic assets to buy foreign currency is a massive bet with a very high cost of being wrong. As your mission control, my job is to make sure your trajectory remains stable.

If the dollar weakens over the next 20 years, your international investments and your diversified stock portfolio are designed to absorb that shock. We manage the risk through tax efficient positioning and making sure your estate plan isn’t tied up in assets that are hard to liquidate.

Brett, you are spot on. Running out and exchanging dollars for euros is not the answer. That’s like trying to jump out of a plane because you saw a cloud. Stay strapped in. Keep your eyes on the long-term flight plan. And remember, if you already own a massively diversified global portfolio of stocks, your craft is already built to handle turbulence just like this.

The final thing I’ll say is the US dollar might not be perfect, but in the global neighborhood of currencies, it’s still the house with the strongest foundation and the best security system, don’t let the headlines move you out of a home that served you well for decades Kudos to you again, Brett, for submitting this very timely question and doing it with an audio submission that is the fast track to get your question answered soon on the show.

So if you’ve got a retirement or a financial question you’d like us to answer, head over to retirement. Isn’t rocket science.com? Click ask a question, or even better, skip to the front of the line by calling Mission Control at 7 0 4 2 3 4 6 5 5 0.

Now let’s broaden our perspective and head over to look at how the Hubble Space Telescope . Has spotted thousands of orphaned star clusters drifting between galaxies.

NASA: In Discovery Houston, we’ve got a good picture of Steve.

Retirement Big Picture

Dr. Chris Mullis, PhD, CFP®: Welcome to the Retirement Big Picture part of our show. This is where we look up and look out to expand our appreciation and understanding of our amazing universe. A Today, I want to talk about a census. Now, usually when we talk about a census. In retirement planning, we’re looking at demographic shifts or tax data, but the Hubble Space Telescope completed a census that was frankly astronomical at scale.

Astronomers used Hubble’s, incredibly sharp vision to count over 22,000 globular star clusters inside a massive city of galaxies called the Coma cluster.

Before we dig into the details of those ancient star clusters, let’s have a little sidebar on the coma cluster. This is a massive collection of over 1000 galaxies, while most of these are elliptical galaxies, which are smooth featureless clouds of old stars.

There are also plenty of spirals and unique. Orphaned star clusters floating in the space between the galaxies, and it’s those orphans that we’re gonna talk about in detail today. Again, back to the coma cluster itself, the host of these orphans, it is roughly spherical. That is the coma cluster of galaxies is roughly spherical in shape and spans millions of light years across because it is relatively nearby in the grand scheme of things of the universe.

It has become one of the most well-documented structures in the history of astronomy. The coma cluster is arguably the most important place in the sky for one reason, dark matter. In the 1930s, a very interesting, quirky astronomer aren’t all astronomers quirky though, but this one was extra astronomer named fritz Zwicky looked at the coma cluster and noticed something strange. The galaxies were zipping around much faster than they should have been based on the amount of visible stuff that’s stars in gas. The cluster didn’t have enough gravity to hold onto these galaxies. They should have flown apart like a merry-go-round.

Spinning too fast. Dr. Zwicky realized there had to be some unseen mass providing extra gravity. He called it dark matter. Today we know that about 90% of the coma cluster is made of this invisible stuff. Now let’s pivot back to the main topic, studying the ancient star clusters. Inside the coma cluster. So these are little cities of stars, actually very big. But compared to the galaxies themselves, they’re very small. These are ancient stars. And for those who aren’t spending your weekends behind the telescope, a gliber cluster is like a cosmic snow globe.

It is a tightly packed ball of several hundred thousand ancient stars in the Milky Way. We have about 150 of them. These are the early homesteaders of the universe that is the oldest members of our galaxy. Think of these clusters, these globular clusters, like the core blue chip investments of a galaxy.

They’ve been there since the beginning. They’ve weathered storms of cosmic collisions, and they provide the foundational structure for everything else.

So what’s really interesting about this census of 22,000 globular clusters in the coma cluster is the story behind the story. It is how this all happened. It wasn’t a single eureka moment from a new photo. It was a project of diligence. Much like the way that many of you have built up , your healthy nest egg, .

The astronomer leading the study, Dr. Juan Madrid actually had his original research project interrupted when Hubble’s advanced camera for surveys had an electronic failure talk about a market crash, but he didn’t give up.

Years later, he and his team, including undergraduate students. Painstakingly pulled together a mosaic of images from the Hubble archives . They took the pieces of data from different programs, sifted through 100,000 potential light sources using algorithms, and identified those 22,000 star clusters based on the star cluster’s, unique aging, red color.

Spherical shape. So it’s a combination of the red color, which tends to reflect older stars and that snow globe, that spherical shape that is so typical of a globular cluster. This is a great reminder that sometimes the most valuable insights come from looking at the data you already have with fresh eyes and sometimes fresh professional eyes.

So you action oriented listeners may be thinking, Hey, I need to go out and see this coma, cluster of galaxies, and maybe I can see the G globular too. So where exactly is this galactic city? Well, it’s located in the Constellation coma, Bari. Now most constellations are named after Heroes or Animals, Orion the Hunter or some major, the Great Bear.

But Coma Barisi has a much more human story. It’s named after Queen Baris II of Egypt. Legend has it that she cut off her long, beautiful hair as a votive offering to the Goddess Aphrodite to ensure her husband’s safe return from war when the hair went missing from the temple. The court astronomers pointed to a fuzzy patch of stars and told the king that the gods had taken the hair and placed it in the heavens.

So let’s talk practical matters. Can you see it? Can you see coma Bari? Good news for our listeners in the United States. The answer is emphatic yes. Coma Bari is a northern constellation. It’s best seen in the springtime. It is located between Leo, the Lion, and B, the herdsman

the constellation itself is visible to the naked eye, though it’s a little faint, kinda like a shiming cobweb of stars. Be forewarned. You won’t see the individual galaxies with your naked eye, so you will need, a decent sized, maybe an eight inch backyard telescope to see the two brightest anchor galaxies of the coma cluster.

So we have nerded out in a lot of details, but why the heck are we talking about this?

Why did Astronomers spend years counting 22,000 balls of Stars? 300 million light years away? Because these clusters are the tracers. They show us how gravity is distorting the fabric of space. By mapping these clusters, we can map where the dark matter is located. Dark matter again, is invisible stuff that makes up most of the universe.

We can’t see it directly, but we can see its effect on everything else. Translating this into our near field universe of retirement planning, there’s a corollary to dark matter. Invisible forces like inflation, sequence of return risk, and tax law changes. You can’t always see them coming, but they are the heavy hitters that determine whether your financial orbit stays on track or drifts off into the void.

Conclusion & Next Steps

Dr. Chris Mullis, PhD, CFP®: We’ve spent today probing the pros and cons of probate and how it does or doesn’t fit into your legacy plans. Now it’s time to open the hatch. This is your space walk. You’re stepping out of the routine and into the bright light to overlay today’s insights on your plans to worry less and retire more.

This isn’t just a stroll. This is where the work gets done to move from theory to better real world outcomes. Here are your next mission Objectives, number one, conduct a titling audit. Review your bank and brokerage statements ensure every account is either titled in the name of your trust or has a valid transfer on death, or a payable on death designation to prevent accidental probate.

Number two, review out-of-state property. If you own real estate in another state, talk to your advisor about ancillary probate. You may need to move that property into a trust or an LLC to avoid having to open two separate court cases in two different states. Number three, draft a digital asset inventory.

Make a list of your online accounts, intellectual property, and even social media handles. Provide your executor or trustee with the authority and the map to access these as these are often the assets that trigger a need for court intervention. And finally, number four, grab your free copy of my Navigating Probate Guide.

You’ll find the link in today’s show notes. In our newsletter and on our website at retirement isn’t rocket science.com/fifteen. I challenge you to take one idea from today’s show and put it into practice this week to make your retirement even better. Thank you so much for joining me. Remember, you’ve done the hard work of saving.

Now let’s do the smart work of planning. Until next time, keep your eyes on the horizon. Enjoy the adventure you are. Go for retirement.

Credits

Dr. Chris Mullis, PhD, CFP®: We thank the National Aeronautics and Space Administration for providing the radio communications between the space shuttle astronauts and the flight controllers.

Disclaimer

This show is for informational and entertainment purposes only. It is not specific tax, legal or investment advice. Before considering acting on anything you hear in this show, first consult your own tax, legal, or financial advisor.